What would a disruptive bank look like?

A while back, I got into a to-and-fro on Twitter with Marc Andreessen and Chris Dixon about banking, which garnered a fair amount of interest and commentary1234, after Marc declared that he is “dying to fund a disruptive bank“.

So far, finance startups have shied away getting their own banking licence, opting to use an existing bank instead. Movenbank and BankSimple talked up their plans to shake up banking but, in the end, both dropped “bank” from their name and partnered with CBW Bank and Bancorp respectively (Simple was subsequently acquired by BBVA). In effect, they built a presentation layer on top of an existing bank. I don’t think that’s the path to the future of banking. Even if you ignore the downsides of building a business on someone else’s platform, I believe that you can’t be truly disruptive unless you build the full stack.

A bank can be broken down into two distinct businesses. The first is the infrastructure required to offer banking services: the banking licence or charter, branches and call centres (increasingly optional), IT systems, ATMs, AML and KYC procedures, connections to domestic inter-bank networks and SWIFT, the ability to issue credit and debit cards, etc. Some of these are revenue-generating (e.g. fees on SWIFT transfers, payment card interchange fees) but, traditionally, retail banks have offered “free” banking to attract customers so that the second business can offer them financial products like credit, overdrafts, loans, savings, investments, pensions, foreign exchange and insurance. This second business has attracted plenty of competition (including startups like Wonga, FundingCircle and TransferWise), but there appears to be little appetite for investing in the infrastructure required to become an actual bank.

The last company to do so in the UK was Metro Bank, which launched in 2010 (the first new high street bank to do so in 150 years) but has failed to make a make a significant impact on the incumbents’ market share (the top four UK banking groups have 70% of the market for personal current accounts5) and is yet to achieve profitability, having racked up over £150m in cumulative losses. With hindsight, part of the reason for Metro’s slow progress is the fact that, rather than trying to disrupt the market, it challenged the incumbents on their own turf by opening high street branches (26 so far, at a cost of over £2m each) and sought to compete on customer service (e.g. Sunday opening and welcoming customers’ pets into branches). Notably, it did not attempt to differentiate itself through technology, opting instead to outsource its IT to Swiss banking systems provider Temenos.

I believe that the technology platform can provide a strategic competitive advantage. As I’ve written before, the lack of competition in the UK market bred complacency and resulted in a failure to innovate and invest in technology (banks are notoriously reluctant to invest in something that doesn’t generate revenue unless it’s mandated by the regulators). As a result, the incumbents’ core banking systems are monolithic, clunky and ill-suited for supporting the kind of services that are made possible by modern consumer technology and connectivity.

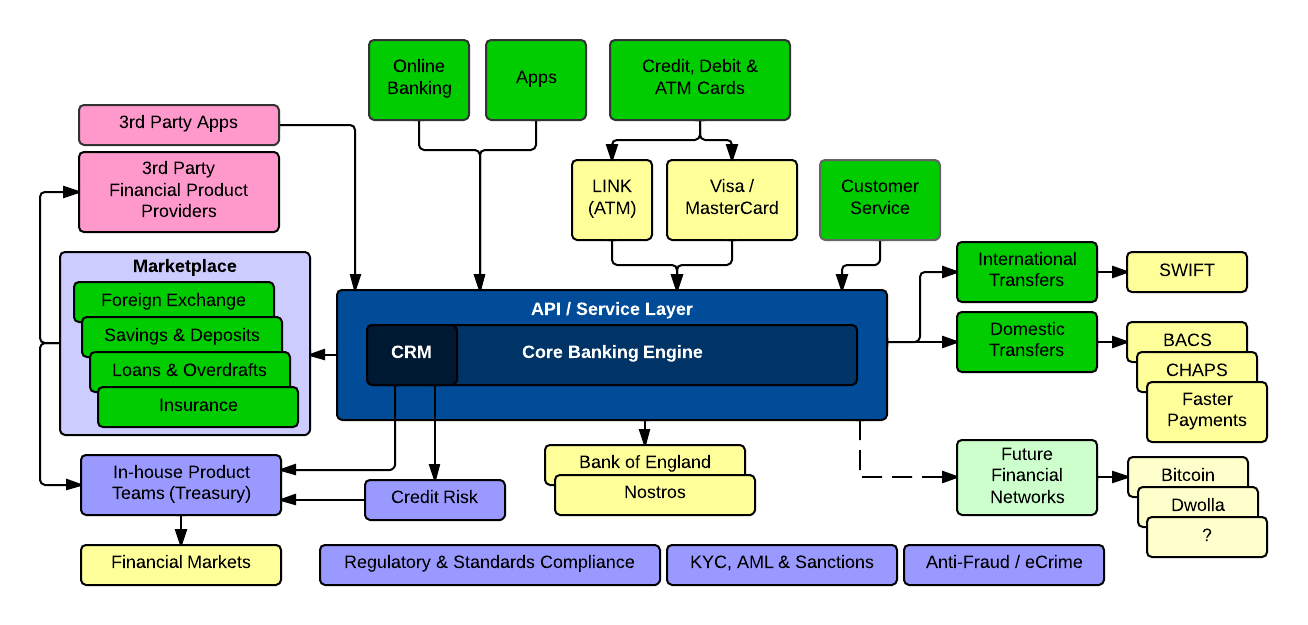

The ability to offer those kind of services would be a key differentiating factor but would require that the new bank build its own platform. I imagine it will look something like this:

A core banking engine, with integrated CRM functionality, wrapped in an API/service layer supporting online banking, and both in-house and 3rd party apps (e.g. personal finance managers, business accounting packages). Building a new engine from scratch, rather than using an off-the-shelf product, will allow the new bank to incorporate new features and functionality, like allowing customers to control which apps have access to their account (in a manner similar to the way Twitter lets you control which apps have access to your Twitter account) and set up IFTTT-style triggers. A modern platform will also make it easy to integrate with new financial networks.

Certain traditional banking services are prerequisites, such as payment cards, access to withdraw cash from ATMs and the ability to send and receive bank transfers both domestically and internationally. However, note the absence of any mention of branches, cheques or accepting cash deposits – all services that are expensive to provide and whose usage is declining precipitously.

Commoditised products like foreign exchange, credit and deposits are a competitive market and it’s easy for customers to access competitors’ product offerings, so it would make sense to create a marketplace where customers can get direct access to 3rd party products as well as those offered by the in-house Treasury product teams. In fact, providing a banking platform-as-a-service and white label services to other financial startups could generate significant revenues.

Efforts by UK regulators to foster competition in the banking market by encouraging more new entrants mean that now is probably the perfect time to launch a bank like this in the UK. In fact, last week brought the news that one of the co-founders of Metro Bank has teamed up with the former chief executive of First Direct (HSBC’s online and phone banking brand) to launch “the UK’s first truly digital bank“, although they appear to be following in Metro Bank’s footsteps by outsourcing the technology platform to Fiserv, a US financial technology provider.

The UK is arguably the best location for a disruptive bank to launch, with a financial technology talent pool that is probably the best in the world, and a sizeable addressable market that’s ripe for disruption. Once established in the UK market, a new bank will be well-positioned to take advantage of the single European market for financial services to expand throughout the EU and, with a tried and tested technology platform, it should be easy to attract the investment required to launch in the US.

The potential rewards are huge but so is the investment needed. Building a new technology platform and putting in place the support structures required is a major undertaking, not to mention the marketing spend that would be required to go mass market. VCs have become used to backing small teams of young technologists who build and launch a business over the course of a three month accelerator programme, or providing growth capital to companies that are scaling a proven business model. Whether they have the risk appetite for a disruptive bank remains to be seen.

- VCs Start Pining to Own a Bank at bankinnovation.net

- To disrupt banking, do you need to own the bank? at qz.com

- Financial interaction: the next generation by Roger Ehrenberg

- If you think ‘rip out and replace our systems’ is naive … think again at thefinanser.co.uk

- Calculated from the 75% quoted by the OFT in their January 2013 Review of the personal current account market less TSB’s 4.3% share after being spun out of Lloyds

“What would a disruptive bank look like?” That is a very interesting question you pose Jack. It is very easy to solve “innovation” with a brand new modern computer infrastructure as you propose. That works for any industry that relies on computer technology. Innovation can come in many forms. You decided to answer for computer systems innovation via a high level schematic. What I find most interesting is you disparage the US company Fiserv who was hired to be technology partner for “the UK’s first truly digital bank,” Atom. Actually, I think you disparaged both of them. If you asked Fiserv what type of company they are I would not be surprised if they answered by saying something like we provide banks “A core banking engine, with integrated CRM functionality, wrapped in an API/service layer supporting online banking, and both in-house and 3rd party apps (e.g. personal finance managers, business accounting packages).” This is how you describe what is needed for a new disruptive bank platform.

The opportunities for a bank of any size in any country to be disruptive are many. Your original question was “What would a disruptive bank look like?”

My questions is, why do you have to replace the entire technology stack to be disruptive?

There are are lot of broken pieces in retail, business and commercial banking today. For example, I am still waiting for an online banking platform that is not rooted in last centuries “check book” and “statement savings” operational focus.

Jack, thanks for writing this article. It is not only time we start thinking differently but to also start acting differently.

@dmgerbino

David Gerbino (@dmgerbino)

April 14, 2014 at 5:00 pm

So, to answer your question (Why do you have to replace the entire technology stack to be disruptive?), I don’t think that the current solutions available (or the legacy systems banks have in place currently) provide a good platform from which to innovate. I’d remind you of Jill Castilla’s recent comment on Twitter: “Core vendors hold banks back in tech innovation more than regs.”

Technologists rarely understand the business’s requirements fully (and business people are rarely capable of understanding technology’s possibilities and limitations, or articulating their requirements in a way that technologists can fully understand), so you end up with technology solutions that limit the business, rather than unleashing it.

jackgavigan

April 15, 2014 at 1:53 pm

@Jack I had a convo with Jill Castilla about vendors [ https://twitter.com/search?q=from%3Admgerbino%20to%3Ajillcastilla&src=typd ]. I agree with her on many levels. Many banks do not/cannot pay for the better bank core product that can integrate with 3rd parties via a published API. What I have observed is many core providers focus on operations and regulations vis-a-vis voice of the customer (VOC) processes and less on future capabilities that #FinTech focused bank workers want or need. The bank vendor space is littered with companies doing truly innovative work. My favorite today is the FICO Falcon product:

Can bank core providers do a better job? Yes. Do they need to rebuild their technology stacks for the realities of today and tomorrow in order to effectively deliver on so called innovative technology? No.

Should bank core technology providers be building a new core product for tomorrow’s banking needs in parallel with keeping their existing products up to date? I think yes. The question is, how many banks and credit unions will be left needing their services.

David Gerbino (@dmgerbino)

April 15, 2014 at 8:22 pm

I’m with Metro and wholly support your statement that they don’t change anything.

Disruption is much more fundamental. It is about rethinking the needs and desires.

Banks grew up as safe places for savings. Then banks sold us the idea of a benign person who controlled your life by lending you money for big things like your house. Both of those models have gone.

So what do we really need/want?

A different system for house purchase – one which is closer to rental or leasing and which is flexible and for life, not tied to one property or being renewed and switched regularly.

We probably don’t need anything for cars, technology etc. – vendors own schemes do the job.

We need much better systems for savings – ones which allow us to invest directly in things we want to support while keeping most of the money safe and explaining the risk/reward system for the rest.

We need a simple way to pay for stuff from the money in our reservoir straight from our mobile or a card. Including moving money to relatives and companies abroad, safely and with guarantees.

This could be integrated with our tax systems, doing our taxes for us & claiming back amounts we are due.

It could also be integrated with our insurances – cars, houses, goods all part of the deal.

It should be integrated with our savings for retirement (pensions are out of date), using that money more effectively.

We don’t need banks. We need simple, effective money management.

The company which provides that – simply easily and on our phone – will disrupt banking totally, irrevocably.

Peter Johnston (@ChallengeThink)

April 15, 2014 at 10:33 am

Great article Jack ! -Rajesh

Rajesh K

April 15, 2014 at 4:13 pm

Jack, great points. Disruptive to me would be more about two critical components: scale and dynamic fulfillment. I don’t need a place or an account just like I really don’t need a drill. I need a hole. I need fulfillment. Sometimes I need cash, sometimes installment, and sometimes revolving. And I get to choose real time or in advance which payment stream “drills” which “hole”. And I want banks to bid on my business real time and dynamically refinance my debt or “buy” my relationship based on factors relevant to the microeconomic and macroeconomic drivers of the day. Each payment stream is calibrated in real time or near real time and I’m updated so I know how big a hole I can drill.

Authorization is driven not by account but by wealth index or aggregate balances. We cherish the account centric world we live in, but it no longer adequately serves the majority of the mass affluent marketplace, which let us admit, is the market the majority of bankers really care about.

However, the account-centric, box-centric model serves the regulators and bankers – all good folks mind you – just fine.

Again, thanks for the great post. It makes one think.

Arp Trivedi

April 15, 2014 at 9:25 pm

Your architecture shows a monolith with an api layer. Hooray. A real difference in the architecture would show “use case silos” that you can mix and match with underlying must have core services for aml, kyc, fraud and risk.

I doubt that the UK is a great place to start that endeavor. From a regulatory perspective you might argue that it is quite business friendly (eventhough the fca is showing more teeth right now than the fsa ever did) but the underlying payment networks like bacs and chaps are a nightmare. Building something on top of that is a waste of time. Fastpay and sepa (why always so uk centric) open up the right path on the transfer side of things. The right market to do this is the us. They are 15yrs behind on banking (they seriously call making a photo of a cheque an innovation). Regulation in the us is a pain but the market is big enough.

Card issuing is or more precisely will be a loss maker with the interchange caps around the corner. This will make your new bank the one that has to charge twice or 3x as much as everyone else gor cards because you can’t subsidise or absorb the costs.

I find it annoying when people state that cash will disappear. How does your sme shopowner get his cash into your bank? Think that your bank will be only consumer facing? Think again. Nobody caters to smes and “speaks” their language and ubderstands their needs. There you have your usp and they are loyal too.

Rafael

April 17, 2014 at 1:03 am

You might be interested in reading about what CommBank, an Australian Bank, are up to. It touches on many of the points you raise.

http://www.brw.com.au/p/lists/50-most-innovative-companies/2013/most_innovative_companies_commonwealth_krYHryj6X4rpWn4hCuRv1J

https://www.commbank.com.au/business/our-innovation.html

stewart

April 17, 2014 at 5:53 am

I put it to you @jackgavigan that actually the issue has more to do with

1) The understanding of new Architectures / or what’s already in the kit bag in senior management

2) A single enterprise “vision” at a Tech AND business model level

3) Most importantly – a three line whip to implement the new Business Model and supporting SDKs

Businesses typically need less “new” silver bullets and more lead bullets.

(Shameful Plug) – partly inspired by this post and one by Mike Butcher, I blogged:

http://www.sytaylor.net/2014/04/21/the-bank-to-developer-b2d-sdk

sytaylor

April 22, 2014 at 11:17 am

You’re listing some of the symptoms of the underlying malaise. Commercial and retail banks certainly can innovate (and some do so surprisingly effectively, in certain areas) but, in my opinion, the lack of competition has meant that there hasn’t been as much pressure to do so as in, for example, the capital markets sector, where competition is far fiercer and the strategic competitive advantage offered by technology has been more apparent and immediate.

jackgavigan

April 23, 2014 at 7:58 pm

Jack, Nice post and comments! We (Open Bank Project) provide an open source API layer (spec and reference implementation on github). Authentication is done by OAuth (as you mention like Twitter, Facebook, Google) so the bank remains gatekeeper of authentication. So far we’ve focused on an API for customer facing Apps (PFM, SME business analytics etc.) but also have a sandbox interface for payments (interested in Ripple etc). We have about 17 apps so far connected to the API. Plus open source starter SDK’s for Node, IOS, Android, etc.

sdredfern

April 25, 2014 at 10:24 am

Great question,

I would look at clay’s christensen theory in order to find an answer: disruption may start in two ways, the first one, called low end disruption, would start with overserverd clients that would love to pay less for a good enough service and the second one, called new market disruption would start in non consumption segments (people who do not have acces to banking systems or circunstances where the current services do not apply). I am afraid that this disruptive bank already exist, just take a look at m-pesa in África or the social Banks like grameen that are building a strong foothold in undeveloped countries.

victorinsight

May 1, 2014 at 1:20 pm

[…] Jack Gavigan answered with this excellent post on a blueprint for a new disruptive bank: https://jackgavigan.com/2014/04/14/disruptive-bank/. […]

Musings on Full Stack Financial Services startups | Tekfin

May 5, 2014 at 10:22 am

I believe part of the reason retail banking is less open is due to the card associations (admittedly South African perspective).

Until the internet came along they were the only international network that connected people doing payments. The internet is a public network that is free to use and this is scary for them. Understandably the associations would prefer the world to continue to pay a transaction fee to use their networks and in return they spend lots of money on marketing and aimless excercises like PCI DSS. As a result they still hold retail payments at ransom and continually make themselves an irreplaceable part of the system by enforcing rules on everyone in the value chain.

Banks today cannot survive without issuing cards from VISA or MasterCard so any bank who wants to encourage a new way for their customers to use their money must hope that this doesn’t piss off their issuing partner. If a bank started processing large volumes of customer transactions without the card networks you can be sure there would be some tough boardroom discussions that followed around acquiring licenses etc.

If we take a step back and simplify consumer payments greatly, every “bank API” must have a means of authenticating the user and linking them to an account on the bank’s host system after that it’s as simple as deciding to authorise the amount requested or not. Today this authentication is done using an identity token (the card) and in some cases a PIN, signature, CVV2 or other factor to prove the card-holder is the card-owner.

What I like about your model is that integration into the card networks is just one of the APIs. Too much “disruption” to date in retail payments still depends entirely on consumers having an association branded card and somehow linking this to the process. (i.e. The account holder’s card is still the gatekeeper to the API)

Replace the card as the authentication mechanism and you have already been hugely disruptive. Banks just need to be encouraged to trust that this can be done securely without the associations. I believe many banks today could add a rich API layer on top of their existing host systems without a full-stack replacement but as with every disruptive force in this industry they are faced with a chicken and egg conumdrum.

“If I allow my account holders to bank using their Facebook account as their auth token who will actually accept that auth token? Is there a standard I can follow so that other banks can do the same and payments acceptros will see the value in supporting this channel?”

What is exciting is that many disruptive players who were dependent on the associations in the past have now cut them out. PayPal started as an email/web auth framework on top of your card but ultimately became a network of it’s own and use’s can have PayPal accounts without needing to have cards.

Personally I see the debit-pull model of consumer payments dying as consumers are increasingly empowered to push payments out of their accounts pro-actively using online tools such as their own bank’s mobile app.

In other words, rather than the merchant requesting funds from the customers bank (debit-pull) let the customer instruct their bank (through a channel both the customer and the bank are comfortable with) to send the money to the merchant (credit-push).

Adrian Hope-Bailie (@ahopebailie)

May 8, 2014 at 3:28 pm

On reflection I realise that I didn’t explicitly point out that a key piece of the payments system are the inter-bank networks and today these are also mostly controlled (at least internationally) by the card associations.

In order for a disruptive bank to be successful they must still be able to “play-nice” with other banks or they effectively become a closed loop system. The associations provide both the consumer-to-bank and inter-bank networks today.

In order for the industry to be disrupted in the way you describe regional and international inter-bank networks will need to emerge that can perform transactions without the need for the association networks.

Ideally this would simply consist of the banks picking a standard for message exchange and using the public internet as their network.

Adrian Hope-Bailie (@ahopebailie)

May 9, 2014 at 8:27 am

Here’s my notes on experiences as a customer since very close to day 1.

OVERALL

Simple does almost everything I want from a basic retail bank. I felt like they had enough access and control to try to solve many of the problems I’d had with other banks. Without the full stack, they still had no shortage of ways to stand out.

COMPLETENESS

I actually wanted fewer internally-maintained features than Simple provided. For example, I didn’t use Simple’s goals at all, though I can see from Twitter comments that some customers did. As another example, Simple’s automatic merchant name cleanup was a minor convenience at best, and had enough errors that I’m not sure it was worth the effort.

Simple had basically reached maturity for a basic retail bank. Yes, there was and is more it could do, but they’re the long tail of retail banking features. (What would an end-to-end reinvention of a bank let them provide that isn’t doable today? Perhaps doing less, not more, and exposing “raw” parts of the stack for a future ZenPayroll or Balanced to consume).

SUPPORT (and paying for it..)

Support made or broke the service to a degree that I didn’t expect, even coming from a bank where I had a personal rep. Simple’s site treats support discussions as the first-class elements they are. The staff is responsive and savvy. It made a huge difference.

I don’t know how interchange fees would cover the costs of Simple’s customer support, let alone software development, ops, and support. Although support was very thorough, Simple didn’t spend a lot of effort turning answers into something that would let other customers find the answer themselves.

Many of my questions were factual topics which could easily go in a FAQ: policies, limits, service features.

Obviously I’d like my bank to be sustainable on the fees it collects, which made it somewhat frustrating when I had to ask a question that didn’t then end up somewhere in Simple’s docs.

This might be a comprehensive FAQ (yes, there’s a FAQ, no, it’s not comprehensive), a public Discourse-style forum, or giving certain customers edit access to the existing FAQ and having staff moderate and release the changes. I think Simple was hoping to differentiate mostly on service, so providing fewer human interactions didn’t really appeal.

It felt like there was a decision here: either they’re a premium bank with a monthly price, or they’re a friend-of-all consumer bank like what WaMu tried to brand themselves as.

Troy

May 21, 2014 at 2:08 pm

[…] So gesehen ist es nur ein logischer Schritt, wenn die Überlegungen, wie man sich eine Bank bauen kann, konkreter und realitätsnäher werden, wie bei Jack Gavigan in seinem lesenswerten Beitrag What would a disruptive bank look like?. […]

Wir bauen uns eine Bank …

May 22, 2014 at 12:56 am

Reblogged this on Innovation in Financial Services.

finservicesinnovation

June 20, 2014 at 8:30 am

Hi guys!

It is a pity that just now I found this great discussion on this very hot topic on ‘disruptive bank look like’!

Let me introduce myself:

I’m João Valentim Bohner, now an independent consultant, who introduced the first ‘Internet’ Banking in this Planet, many years before the true Internet was born.

It was on Feb. 16, 1981 in Viena, Austria.

The Bank was the Citicorp branch in Viena and the client was the Voest Alpine, a steel company.

Since then I’m on the quest for the ‘ideal’ business banking Architecture.

And, I think, I’m almost coming there!

But let’s go back at that time.

At that time there were no databases engines, there were no modems, no PCs,etc. only terminal emulators. But we did it!

The great hero wasn’t the communication via public net, although communication has collaborated heavily and obviously with great creativity in its implementation.

The GREAT HERO was the integrated, online, and real-time ‘core system’ implemented in the Bank (1980) allowing the client make queries, see balances, make transfers, make foreign exchanges, etc. updated. And this was possible because there were an OS, called BOSS, that allowed to handle indexed files by ‘things’ indexes, like customer, account, currency, etc.

That was the starting of a bandwagon followed by many banks in various forms, by phone, with huge batch updated DWs, even with Videotext (Remember? It was a kind of text with some graphics capabilities).

Nowadays Internet Banking is part of our day’s life and nobody remembers the true GREAT HERO.

Now, as Jill Castilla recently commented on Twitter:

“Core vendors hold banks back in tech innovation more than regs. Our options are horribly limited.”

That’s the purest true!

And worst: You have no option!

Each today’s vendor proposal is to exchange six for half-a-dozen!

Something similar to what has happened in the early 80’s is happening now.

The GREAT HERO is missing.

Many ‘cosmetics’ (smartphones, iXXXs, wearables, beacons, NFCs, Intelligent ATMs, geopositioning, etc.) are popping up.

And the bandwagon now is called ‘payments’, even if ‘payments’ are just a little part of the full Banking Business.

So,with the development of “The Bank of the Future” Architecture, in course, I can drop a few hints about “What would a disruptive bank look like?”:

– No more ‘core systems’ as those of today. Financial activities are processed corporately, completely, accurately and definitely on time of the events.

– No more information islands and DWs. All information for the Bank, for the channels, for the customers, for the regulations, for BI, among others are obtained from a single source of knowledge.

– No more islands of processing. All financial events are processed corporately through a single ‘cloud engine’. (This is due to the BOA – Business Oriented Architecture).

– No more business dependency on technology. New products are created by business staff combining ‘business components’ and ‘business processes’ which are recognized by the ‘cloud engine’. One day time to implement a new product.

– No more complex navigation menus, on the customer’s terminals. The full financial relationship between customer and the bank is shown on the first page. Customers see details of its financial activities and make transactions, by drilling down on the corresponding summary item.

– No more high budget just to maintain ICT. A drop – at least – 10 times current operational costs (not 10%).

– No more end-of-day stops. The local-time clock triggers end-of-day balances stamping for each branch of each country.

– No more ‘releases’. The “Bank of the Future” is updated by adding/replacing business components. (The replaced component will still be valid for back value purposes on its period).

– There are many, many others…

I’d like your feedback on this ‘answer’ and I’m open and very interested in discussing this exciting matter!

JVB

joao.bohner@gmail.com

Joao Valentim Bohner

September 30, 2014 at 12:19 am

Jack,

I disagree that you need to build the full stack. The books industry and music industry were massively disrupted without Amazon needing to publish every book, or Apple iTunes needing to hire bands and recording studios.

While technologies like the blockchain will ultimately disrupt the banking rails, the biggest issues with banking today revolve around poor CX burdened by a legal and compliance led view of customer interactions. In this respect you can revolutionize the distribution layer of banking without needing to build the whole stack. In fact, the reason you shouldn’t is that as a chartered bank and owning the full stack you have less flexibility on the CX than if you hook into the ecosystem as a disruptor. Regulators are much tougher on the stack owners than on partners and program mangers.

Key, however, is a bank partner willing to let you push the boundaries.

Here’s another error in your line of reasoning. Start ups in this space aren’t trying to disrupt the bank end to end, they’re just trying to take a specific chunk of functionality or experience and disrupt that, so owning the stack is overkill. The reason no one wants to build a digital pure play bank end to end is that banking has become an amalgam of lots of complex systems and processes, many of which are independent silos and unrelated. To fix this you need to deconstruct these silos into discreet services ans optimize them.

It seems you’re looking for a digital version of Chase or BofA powered by Bitcoin and the blockchain. That’s not what is going to get us there. Rethinking the context of banking and redefining those experiences independent of the traditional stack is what is necessary

Brett King

Moven

Brett King

November 25, 2014 at 3:03 pm

I would say that Amazon disrupted bookstores, not publishers. Apple disrupted record stores, not record companies. Both those companies created distribution platforms that stand head and shoulders above the competition. If you look at the left hand side of my diagram, you’ll see a section tagged Marketplace – that’s the financial equivalent of the App Store or iTunes, where third parties can offer financial products through the disruptive bank’s distribution channel.

There are two problems with building on someone else’s platform. First, you inherit their platform’s limitations. Second, you’re reliant on their willingness to continue the partnership. At any point, they could replicate your offering and terminate the partnership. Both Facebook and Twitter have done this in the past – they let third-party developers innovate on their platforms and, when the successful application use cases became clear, they focused on those areas and dispensed with the competition by pulling the rug out from under large parts of the eco-system.

Here in the UK, there are at least two companies looking to do exactly that: Atom and Starling.

Or, as my old boss at Morgan Stanley used to say, “Reduce the incremental cost per trade to as close to zero as possible, and pump up the volume!”

It’s entirely possible to optimize most processes in banking to the point where they can be automated, and processed in real-time but I believe that anyone who tries to do so on top of a legacy technology infrastructure is handicapping themselves from the outset by building on shaky foundations.

Absolutely not! In fact, I’m quite the Bitcoin skeptic!

I’ve spent most of my career working in capital markets (i.e. trading) technology, where fully automated, real-time processing is common, and technology is so critical that the lines between “the Business” and “IT” are often blurred. I’ve then had the opportunity to apply that same approach in a retail and commercial banking context (FX and international payments), and the result was a real eye-opener. My expectation is that, sooner or later, someone’s going to do the same for the rest of the banking stack. I don’t think the incumbents are best-positioned to do it because (a) they have their legacy platforms and businesses to distract them, and (b) they don’t view technology as an integral and critical part of what they do, or as a means of gaining a strategic competitive advantage.

Incidentally, the latter factor is the reason I don’t expect Atom – who are outsourcing all their technology – will be a disruptive bank. Outsourcing makes it impossible to achieve synthesis between the business and technology. That, in my opinion, is why you need to build the full stack.

In fact, I expect that the disruptive bank will look more like a tech company than a bank as we know it today.

jackgavigan

November 25, 2014 at 5:04 pm

Gentlemen,

that is a great discussion – which to some parts I already had several times with Brett 😉

The core-sentence to me in your comment, Brett, is: “Rethinking the context of banking and redefining those experiences independent of the traditional stack is what is necessary”.

I think, we do not really disagree on that sentence itself. But I think we have a different idea about the “preconditions” to come to that ambitious point of creating banking more contextual. The tech-stack inculding a banking license is crucial. In my understanding, you must be in charge of your tech stack including the allowance to run own products and services – otherwise it is as Jack said: you are (awfully) dependent from your corebanking-partner. How to deliver “real contextual banking” if you cannot service a loan in 60 seconds on a saturday evening, simply because this particular corebanking is not capable executing something like that?

As simple as that: You have to sit in plane if you really want to hijack it?

Matthias (CEO FIDOR BANK)

matthiaskroener

November 25, 2014 at 5:16 pm

Stay tuned.

At Moven we’re going to show you a disruptive model with far greater scale than what you’re proposing here. The key problem is even if you own the stack you are limited to geographies by nature of regulation. I think we’ve cracked that problem and we have a way to provide a revolutionary bank account that is used by millions of people in 30-40 countries in the next couple of years.

The stack would not get you there without massive capital investment, or model will.

In short if you want to create a model used by 100m people you have to split distribution and manufacturing

BK

Brett King

November 25, 2014 at 6:41 pm