Archive for April 2014

Vesting: Just Do It

I would advise the founders of any startup to ensure that all founders’ equity is subject to vesting. Failure to do so can cause massive problems.

I would advise the founders of any startup to ensure that all founders’ equity is subject to vesting. Failure to do so can cause massive problems.

Rather than reinvent the wheel, I’ve put together some key quotes from – and links to – relevant articles by people who are far more knowledgable and qualified about the topic than I.

What would a disruptive bank look like?

A while back, I got into a to-and-fro on Twitter with Marc Andreessen and Chris Dixon about banking, which garnered a fair amount of interest and commentary1234, after Marc declared that he is “dying to fund a disruptive bank“.

So far, finance startups have shied away getting their own banking licence, opting to use an existing bank instead. Movenbank and BankSimple talked up their plans to shake up banking but, in the end, both dropped “bank” from their name and partnered with CBW Bank and Bancorp respectively (Simple was subsequently acquired by BBVA). In effect, they built a presentation layer on top of an existing bank. I don’t think that’s the path to the future of banking. Even if you ignore the downsides of building a business on someone else’s platform, I believe that you can’t be truly disruptive unless you build the full stack.

A bank can be broken down into two distinct businesses. The first is the infrastructure required to offer banking services: the banking licence or charter, branches and call centres (increasingly optional), IT systems, ATMs, AML and KYC procedures, connections to domestic inter-bank networks and SWIFT, the ability to issue credit and debit cards, etc. Some of these are revenue-generating (e.g. fees on SWIFT transfers, payment card interchange fees) but, traditionally, retail banks have offered “free” banking to attract customers so that the second business can offer them financial products like credit, overdrafts, loans, savings, investments, pensions, foreign exchange and insurance. This second business has attracted plenty of competition (including startups like Wonga, FundingCircle and TransferWise), but there appears to be little appetite for investing in the infrastructure required to become an actual bank.

The last company to do so in the UK was Metro Bank, which launched in 2010 (the first new high street bank to do so in 150 years) but has failed to make a make a significant impact on the incumbents’ market share (the top four UK banking groups have 70% of the market for personal current accounts5) and is yet to achieve profitability, having racked up over £150m in cumulative losses. With hindsight, part of the reason for Metro’s slow progress is the fact that, rather than trying to disrupt the market, it challenged the incumbents on their own turf by opening high street branches (26 so far, at a cost of over £2m each) and sought to compete on customer service (e.g. Sunday opening and welcoming customers’ pets into branches). Notably, it did not attempt to differentiate itself through technology, opting instead to outsource its IT to Swiss banking systems provider Temenos.

I believe that the technology platform can provide a strategic competitive advantage. As I’ve written before, the lack of competition in the UK market bred complacency and resulted in a failure to innovate and invest in technology (banks are notoriously reluctant to invest in something that doesn’t generate revenue unless it’s mandated by the regulators). As a result, the incumbents’ core banking systems are monolithic, clunky and ill-suited for supporting the kind of services that are made possible by modern consumer technology and connectivity.

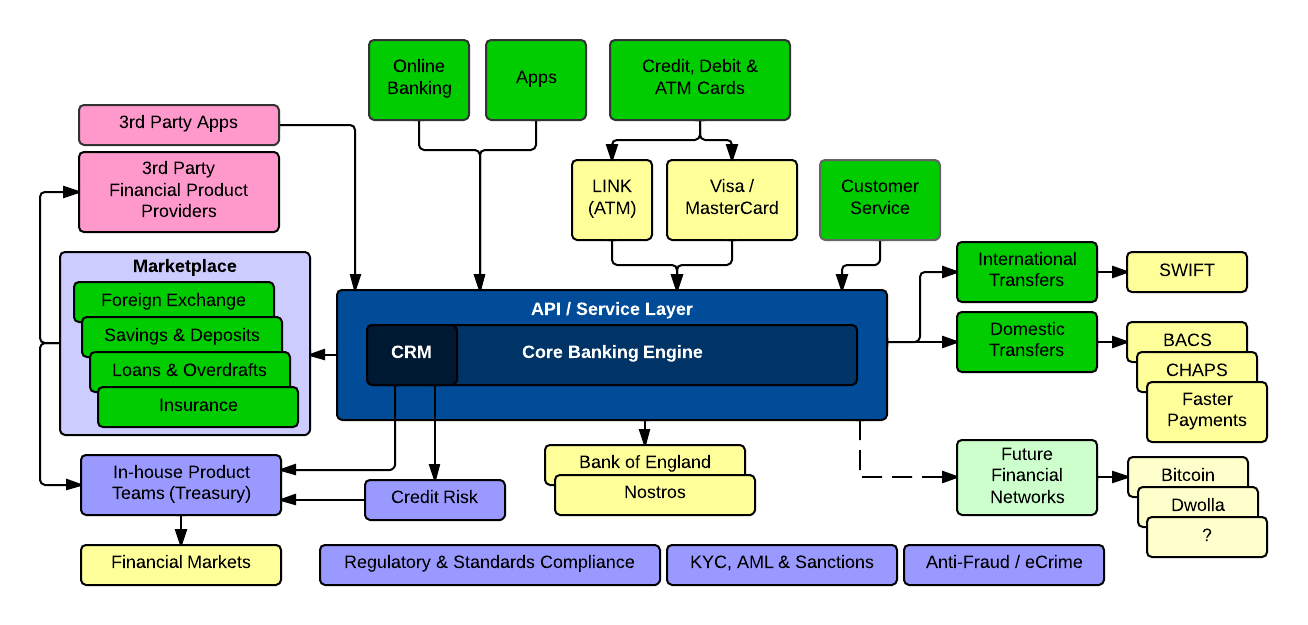

The ability to offer those kind of services would be a key differentiating factor but would require that the new bank build its own platform. I imagine it will look something like this:

A core banking engine, with integrated CRM functionality, wrapped in an API/service layer supporting online banking, and both in-house and 3rd party apps (e.g. personal finance managers, business accounting packages). Building a new engine from scratch, rather than using an off-the-shelf product, will allow the new bank to incorporate new features and functionality, like allowing customers to control which apps have access to their account (in a manner similar to the way Twitter lets you control which apps have access to your Twitter account) and set up IFTTT-style triggers. A modern platform will also make it easy to integrate with new financial networks.

Certain traditional banking services are prerequisites, such as payment cards, access to withdraw cash from ATMs and the ability to send and receive bank transfers both domestically and internationally. However, note the absence of any mention of branches, cheques or accepting cash deposits – all services that are expensive to provide and whose usage is declining precipitously.

Commoditised products like foreign exchange, credit and deposits are a competitive market and it’s easy for customers to access competitors’ product offerings, so it would make sense to create a marketplace where customers can get direct access to 3rd party products as well as those offered by the in-house Treasury product teams. In fact, providing a banking platform-as-a-service and white label services to other financial startups could generate significant revenues.

Efforts by UK regulators to foster competition in the banking market by encouraging more new entrants mean that now is probably the perfect time to launch a bank like this in the UK. In fact, last week brought the news that one of the co-founders of Metro Bank has teamed up with the former chief executive of First Direct (HSBC’s online and phone banking brand) to launch “the UK’s first truly digital bank“, although they appear to be following in Metro Bank’s footsteps by outsourcing the technology platform to Fiserv, a US financial technology provider.

The UK is arguably the best location for a disruptive bank to launch, with a financial technology talent pool that is probably the best in the world, and a sizeable addressable market that’s ripe for disruption. Once established in the UK market, a new bank will be well-positioned to take advantage of the single European market for financial services to expand throughout the EU and, with a tried and tested technology platform, it should be easy to attract the investment required to launch in the US.

The potential rewards are huge but so is the investment needed. Building a new technology platform and putting in place the support structures required is a major undertaking, not to mention the marketing spend that would be required to go mass market. VCs have become used to backing small teams of young technologists who build and launch a business over the course of a three month accelerator programme, or providing growth capital to companies that are scaling a proven business model. Whether they have the risk appetite for a disruptive bank remains to be seen.

- VCs Start Pining to Own a Bank at bankinnovation.net

- To disrupt banking, do you need to own the bank? at qz.com

- Financial interaction: the next generation by Roger Ehrenberg

- If you think ‘rip out and replace our systems’ is naive … think again at thefinanser.co.uk

- Calculated from the 75% quoted by the OFT in their January 2013 Review of the personal current account market less TSB’s 4.3% share after being spun out of Lloyds