Archive for the ‘Fin.Tech’ Category

Brexit’s Impact on London’s Tech Startup Sector

Now that the dust has settled on last weeks’ referendum, it’s becoming increasingly apparent that Brexit will actually happen, raising the question of what the implications are for London’s tech startup sector. Some are saying that Berlin, often cited as London’s biggest rival for the title of Europe’s startup capital, stands to benefit from Britain’s withdrawal from the EU.

Others reckon that, to paraphrase Marc Andreessen, free from EU red tape, it’s entirely possible that Brexit will make the UK a more attractive place to build and finance new technology companies. It certainly seems likely that the regulatory burden on businesses in the UK will be reduced considerably, and the absence of the UK’s moderating influence may well mean that businesses within the EU will be subject to more regulation than they would have been if the UK remained.

However, this impact isn’t likely to be felt for at least several years after the UK leaves the EU (which is unlikely to happen before October 2018). For me, the two key factors in the short to medium term are access to talent and London’s status as Europe’s financial capital.

As part of the EU, London has been able to draw on a huge pool of talent from across the continent. Young, tech-savvy talent has been able to move to London without having to worry about visas or immigration restrictions. Dissatisfaction with the level of net migration into the UK (and, in particular, the pressure this has placed on the UK’s public services) was a key factor in the referendum result, so it seems likely that restrictions on immigration will be put in place after the UK leaves the EU. The greatest restrictions are likely to be imposed upon unskilled migrants.

However, the UK government has long recognised the importance of being able to attract skilled talent, as evidenced by its inclusion of “digital technology” amongst the areas of expertise that are eligible for the Tier 1 (Exceptional Talent) visa. Therefore, it seems highly likely that a system will be put in place to maintain London’s attractiveness as a destination for graduates and other suitably skilled talent from the EU. Critically, the current visa scheme does not require that the applicant has a job offer, meaning that successful applicants can work for themselves or start a new company.

If the application process can be simplified, streamlined, and made less expensive (ideally, it should be as simple as applying for an ESTA to visit the US), there’s no reason why London shouldn’t continue to attract talent from across Europe.

London’s success as a financial capital might appear orthogonal to its success as a tech startup hub. Some view the financial sector as a source of competition for tech talent but the truth is more nuanced. A lot of talent is attracted to London because of the financial sector, adding to London’s talent pool. Many tech startups recruit people who have worked for banks or brokerages. It also provides a safety net for tech talent whose startup is unsuccessful. The perceived risk of starting a new company (or taking a role with a startup) is lower if you can be confident of being able to find contract work in the City if it doesn’t work out. This effect is obviously strongest in the fintech sector but I believe it applies across the wider tech sector.

As a financial capital, London is also a nexus for investment capital. Many VC funds are based here, and the UK has spearheaded equity crowdfunding, with a permissive regulatory environment and tax breaks for individuals investing in early stage startups. If London’s financial institutions are forced to move part of their operations to Europe, London’s economy will take a hit (probably similar in scale to – but lancer-lasting than – the post-2008 economic downturn) and there will be less capital available for early-stage companies. Large banks have already begun making contingency plans to relocate jobs and functions to Dublin, Paris or Frankfurt. The key determinant will be the extent to which the UK retains access to the single market for financial services after it leaves the EU and, in particular, whether UK institutions will retain the “passporting” rights that allow them to offer services across the EU from a UK base.

On the one hand, it seems unlikely that the EU will offer such a concession. The French in particular have long been disgruntled that London remained Europe’s financial capital, despite being outside the Eurozone. However, for the UK government, minimising the impact to the City of London will be a top priority, as the employment and tax revenues it generates make an important contribution to both the UK economy and the UK’s public finances.

Fortunately, the UK has a strong hand to play in the negotiations that will follow the activation of Article 50. The UK imports far more from the EU than it exports to the EU. The German and Dutch economies would take a major hit if trade barriers were erected between the UK and the EU. Therefore, it seems likely that the UK government will seek to negotiate a deal that allows UK financial institutions to retain full access to the EU market, in exchange for allowing European exporters to retain access to the UK market. If such a deal is struck, the impact on London’s financial sector will be minimal.

Fortunately, the UK has a strong hand to play in the negotiations that will follow the activation of Article 50. The UK imports far more from the EU than it exports to the EU. The German and Dutch economies would take a major hit if trade barriers were erected between the UK and the EU. Therefore, it seems likely that the UK government will seek to negotiate a deal that allows UK financial institutions to retain full access to the EU market, in exchange for allowing European exporters to retain access to the UK market. If such a deal is struck, the impact on London’s financial sector will be minimal.

Many other factors that have contributed to London’s success as a tech hub won’t be impacted by Brexit at all. Whether or not we’re in the EU, the UK is still one of the largest economies in the world. London will remain one of the great cities of the world, with the attendant economies of scope. London’s universities will continue to rank among the best in the world, contributing an endless stream of graduates to the city’s talent pool. London will remain a welcoming and cosmopolitan city, and English will remain one of the world’s most widely-spoken languages.

There’s also the prospect that leaving the EU will open up a host of other opportunities for the UK and London. Less red tape seems likely to reduce the cost of doing business here. Freedom from EU constraints will allow the UK to negotiate bi-lateral deals with other, emerging economies. We could even see the UK joining NAFTA to form a North Atlantic Free Trade Association. What we currently perceive as a crisis may well prove to be the source of endless opportunity.

In the short-term, we’ll probably hear more anecdotes about spooked VCs withdrawing investment offers to UK startups but as things settle down over the coming weeks, I expect we’ll return to business as usual. So, to quote Hussein Kanji, keep calm and carry on.

Why I think TheDAO is a Success

The usual plague of so-called “experts” have come out of the woodwork following today’s attack on TheDAO, to tweet, blog and bloviate their hindsight-informed opinions about TheDAO’s “failure” and the implications for the future of smart contracts (despite the fact that most of them barely can barely string together a coherent description of what a smart contract is, let alone write one).

I don’t view TheDAO as a failure. I view it as an experiment that has reached its conclusion. We learnt something important today – we learned that this particular configuration of a DAO doesn’t work. Future DAOs and smart contracts will be better because of what we’ve learned, from the specific bug that the attacker tried to exploit, to the insights we’ve gleaned into voting incentives and DAO governance. We’ve learnt a lot about the benefits of being able to upgrade smart contracts after they’ve been deployed, and the lawyers and regulators have plenty of food for thought and debate, with all the legal questions that have been raised by both TheDAO itself and the proposed use of a hard fork to return investors’ ether.

It’s very easy to criticise the Slock.it team but they got a lot of things right and it appears that, in the end, all TheDAO’s investors will get their ether back (albeit with the assistance of the Ethereum community in implementing a hard fork). That’s no mean feat and they deserve credit and respect for what they achieved.

Most experimentation and innovation happens in private, and all the wrinkles are ironed out long before the final product is unveiled. However, in this area – cryptocurrencies, blockchains, smart contracts and DAOs – the experimentation and innovation is happening in the open.Bitcoin wasn’t invented in a corporate R&D lab. Ethereum was funded by the venture crowd, not a venture capitalist. The downside is that we get to see how the sausages are made and any mistakes are public, but the upside is that anyone can participate, and the degree and pace of innovation – its velocity, for want of a better term – is far higher as a result.

Most experimentation and innovation happens in private, and all the wrinkles are ironed out long before the final product is unveiled. However, in this area – cryptocurrencies, blockchains, smart contracts and DAOs – the experimentation and innovation is happening in the open.Bitcoin wasn’t invented in a corporate R&D lab. Ethereum was funded by the venture crowd, not a venture capitalist. The downside is that we get to see how the sausages are made and any mistakes are public, but the upside is that anyone can participate, and the degree and pace of innovation – its velocity, for want of a better term – is far higher as a result.

If we want to reap the benefits of open innovation, we also have to embrace the downsides, including the experiments that we learn from, even when the outcome isn’t what was expected or hoped for; we have to applaud those who try, even if they don’t succeed; and, above all, we should elevate those who do above those who merely talk, tweet and blog.

I invested a small amount of money in TheDAO because I believe that the best way to learn is to get involved and put some skin in the game. If I never get the money back, it will have been a small price to pay for the amount I’ve learnt. If I do get it back, then I hope that I’ll have the opportunity to invest it in TheDAO v2 so we can have another try and see if we can’t learn a bit more.

Towards an Open Banking API Standard

Disclaimer: I am a member of the Open Banking Working Group (OBWG) and was involved in drafting the OBWG report. However, the thoughts and opinions presented here are strictly my own.

The OBWG’s report was published yesterday with the somewhat misleading title The Open Banking Standard. We’re a long way from a standard but this report is a significant step along that path. Its purpose is to lay out a roadmap for defining an Open Banking API standard that can achieve widespread adoption, and to put forward some strawman proposals, intended to generate discussion of their merits and weaknesses, with the objective of generating new and better proposals.

The OBWG’s work follows on from the Fingleton report, which looked at the potential benefits of banking APIs and open data, and HM Treasury’s public consultation on data sharing and open data in banking.

The OBWG was convened with three core objectives:

- Deliver a framework for the design of an open API standard in UK banking focussing on personal and business current accounts;

- Evaluate how increased levels of open data in banking can benefit consumers, businesses and society; and

- Publish recommendations in a paper by end of 2015 outlining how an open API standard can be designed, delivered and administered, alongside a timetable and implementation roadmap for achieving this

It’s important to note that this initiative is separate from – and has a wider scope than – PSD2. However, I would predict with a high degree of confidence that the functionality required to fulfil PSD2’s requirements will form part of the Open Banking API Standard, and I would not be surprised if the UK implements PSD2 by mandating compliance with the Open Banking API Standard.

One of the key challenges in coming up with such a standard is to figure out how banking APIs can be opened up to third parties while ensuring that consumers are adequately protected against fraud and banks aren’t unreasonably held liable for third parties’ failings. Currently, banks control the technology channels that their customers use to access their accounts electronically. Online banking is through the bank’s own website; mobile banking is through the bank’s own app. Liability for any losses rests with either the bank (if their security proves inadequate) or the customer (if they fail to take the necessary security precautions). Opening up banking APIs and granting access to third parties complicates that picture and banks are understandably wary.

The proposals presented in the report comprise a combination of provisions (including an OAuth-based authentication and authorisation model, and vetting and licensing of third parties) that represent a compromise somewhere between completely open access that would allow even hobbyist programmers to create apps that connect to banks’ APIs, and a overly-restrictive regime with requirements or costs that are too onerous for finch innovators and startups. One aspect that I’m a particular fan of is the idea that API functionality should be permissioned atomically, and that the security standards to which the third party will be held and the scrutiny to which they will be subjected should be commensurate to the level of access they wish to obtain. For example, a startup wishing to offer a personal financial management solution, which requires “read-only” access to accounts would be subject to less onerous requirements than a company seeking access to instruct payments from their customers’ accounts.

I have set up a mailing list to facilitate discussion of the report and future developments in this space. Instructions on how to join the list can be found here.

Fundamentally, I believe that the UK fintech sector will benefit hugely if we can make rapid progress towards an Open Banking API standard, and I believe that there’s an opportunity for the UK to take a leadership role, in the same way that it did in information security standards, with the adoption of BS7799 as ISO27001.

It’s entirely possible that neither the banks nor fintech innovators will be entirely happy with the report’s proposals. If so, then I think we’ve done a good job. Personally, I think it’s a significant step forward and I hope to remain involved at the next stage of establishing an implementation entity to take the concept forward.

UK Government Outlines Support for FinTech and Digital Currencies

Yesterday was a significant day for FinTech in the UK. Having previously made it clear that the government wants to make London the leading location for the FinTech and digital currencies sectors, the Chancellor, George Osborne, used the Budget to lay out more details of how the government intends to achieve that.

The Government Office of Science also released its Blackett review into FinTech, and HM Treasury published both their response to the call for information on digital currencies that they launched last November, and a policy paper outlining the government’s strategy for delivering competition and choice banking.

I highlight some of the key announcements from the Budget below.

Promoting competition is one of the FCA’s three objectives (the other two are protecting consumers and protecting financial markets) and, fortunately, its leadership fully recognises both the role that innovation can play in driving competition, and the fact that regulation can be a significant barrier to innovation. Project Innovate is an initiative launched last August to help innovator companies navigate regulatory hurdles and bring new products and services to market.

One of the key challenges is that existing regulations often don’t cover emerging business models. Even when they do, startups often lack the resources to achieve full compliance. Hopefully, the FCA will be able to come up with a sandbox model that allows innovators to pilot new products, services and business models that they would otherwise struggle to bring to market.

Just as technology is transforming the way financial services are delivered to customers, it has the potential to transform the way regulation is delivered and reduce regulatory costs. By taking the lead in this area, the FCA and PRA can make the UK a more attractive regulatory regime and provide a fertile environment for UK companies to develop ‘RegTech’ products and expertise that can be exported overseas.

In Germany, the widespread adoption of the HBCI/FinTS banking API has helped foster a strong FinTech sector, spawning startups like Fidor Bank, Figo, Number26 and Avuba, as well as the Open Bank Project. If the UK banking sector can be persuaded to adopt a similar API, it can only be a positive development for UK FinTech.

The Bank of England has taken a keen interest in digital currencies and blockchain technology, and even raised the question of “Why might central banks issue digital currencies?” in a recent discussion paper. HM Treasury launched a call for information on digital currencies last November, and released a detailed response to the feedback alongside the Budget yesterday. The paragraphs below (with numbers in red) are taken from the latter document.

The government clearly perceives a significant opportunity in this space but the key challenge is to ensure consumer protection and prevent the use of digital currencies for criminal purposes (including money laundering and terrorist financing) without stifling innovation.

There’s little doubt that here in the UK, lack of regulation has hampered the digital currencies sector. Banks, having been hit with punitive fines in the past for failing to do enough to prevent money-laundering, refuse to touch anything Bitcoin-related with a 10-foot bargepole, meaning that UK companies in this space are typically forced to bank overseas (e.g. Bitstamp, Coinfloor and CEX.IO bank in Slovenia, Poland and Latvia, respectively, despite being based in the UK). Applying AML regulation to exchanges should remove this barrier to banking services and help make the UK a more attractive regulatory regime.

The next Parliament will begin in May so, with luck, we will see the result of this consultation by the end of the year.

The new Payment Systems Regulator may also have a role to play in ensuring that that digital currency businesses are not excluded from payments networks by UK banks.

BSI is the UK’s national standards body. As well as safety standards for things like crash helmets and seatbelts, it pioneered the quality assurance and information security standards which formed the basis of the ISO 9000 and ISO/IEC 27000 series, respectively.

The digital currency sector has seen its fair share of fraud, ponzi schemes and fiduciary failures, so it’s interesting to see the UK government opting against prescriptive regulation to protect consumers, in favour of giving the sector the opportunity to self-regulate. It’s very much a pro-innovation stance, and stands in marked contrast to the approach taken by the New York Department of Financial Services – it’s possible that the UK government, having seen the negative reaction to the New York Department of Financial Services first BitLicense draft, saw an opportunity to steal a march on New York (which vies with London for the title of the world’s leading financial capital).

It’s worth bearing in mind that “self-regulation” has a decidedly mixed track record in the UK, so there’s a question-mark over whether this approach will engender enough consumer confidence to support mainstream adoption. Also, the use of the phrase “at this stage” is significant.

The £10m in funding for research is a relatively small but significant indication that the government is willing to put its money where its mouth is. The Research Councils are the primary source of funding for research in the UK. The Alan Turing Institute is a newly-formed organisation intended to support research in Big Data and algorithms. Digital Catapult is an Innovate UK initiative intended to help commercialise data innovation.

Concentration of talent plays a key role in the formation of industry clusters. If the UK can attract talent to conduct research, and provide a fertile environment for commercialising the fruits of that research, it stands a very good chance of establishing a strong digital currency cluster.

FinTech is a significant contributor to the UK economy, and are are a key element of London’s role as a global financial centre. Yesterday’s announcements are a clear sign that the government is not just paying lip service when it says it wants the UK to be the best place in the world to do business in this sector.

The prospect of being formally regulated will likely prove highly attractive to companies focusing on Bitcoin and other digital currencies. It will confer legitimacy, and give both customers and investors greater confidence in the sector. Passporting will also give companies regulated in the UK the ability to offer their services across the rest of the EEA.

We’ve already seen companies like CoinJar move to the UK because of its Bitcoin-friendly tax regime. I wouldn’t be surprised if others follow in its footsteps.

I’m interested in hearing other’s thoughts on yesterday’s announcements. Please leave your feedback below as a comment or contact me directly.

The State of the Blockchain in 2015

During 2014, nearly 1.6m bitcoins were mined and more than 25m Bitcoin transactions were written to the Blockchain, which doubled in size, ending the year at 26.4GB. The ongoing growth in transaction volumes has led to a renewed focus on Bitcoin’s scalability issues.

During the same period, the price of Bitcoin dropped by more than 50%, causing the growth of the network’s hashrate to slow towards the end of last year, which triggered the first drop in difficulty since early 2013. Last month (coincidentally as the trial of Ross “Dread Pirate Roberts” Ulbricht got underway) the Bitcoin price dipped below $200 for the first time since November 2013, prompting some sizeable mining pools to suspend operations. The implication is that the mining hardware arms race has squeezed profit margins to the point where some miners are unprofitable when the price drops below $200 (i.e. value of the bitcoins generated by the mining hardware is less than the cost of electricity required to power it). The fact that some miners are suspending operations instead of continuing to mine and simply hanging on to the bitcoins mined until the price rises again suggests that they may lack the (fiat currency) funds to keep paying for electricity or that they’re fearful that the price won’t recover and they’ll end up permanently in the red.

For now, the question is moot, as the price has recovered to ~$225 (giving the ~14m bitcoins in circulation a total value of ~$3.15bn), but it will be interesting to see what happens if the price drops again.

In March, Newsweek relaunched their print edition in March with a cover story claiming that that they had unmasked Dorian Nakamoto as the creator of Bitcoin. The man in question denied having anything to do with Bitcoin and the real Satoshi Nakamoto surfaced online to declare: “I am not Dorian Nakamoto.”

The first really big Bitcoin bankruptcy took place in February when MtGox shut down and filed for bankruptcy, claiming that hackers had stolen 850,000 bitcoins (worth around $460m at the time) and that $28m was “missing” from its bank accounts. It later emerged that 200,000 bitcoins were found in a “forgotten” wallet and, nearly a year later, the saga has yet to be fully resolved.

Of course, MtGox wasn’t the only Bitcoin bankruptcy: Flexcoin and Bitcoin Trader shuttered after being hacked, Neo & Bee collapsed amid suspicions of fraud, and London-based MintPay and Moolah closed down after CEO “Alex Green” (subsequently revealed as an alias of Ryan Kennedy) absconded with over $1.4m worth of bitcoins.

Unfazed, VCs invested more than $300m in Bitcoin startups during 2014 and if Coinbase’s $75m round in January is anything to go by, that trend seems set to continue in 2015. It’s clear that some VCs believe that Bitcoin and the Blockchain represent a “New World”-style opportunity (similar in nature to the Internet itself back in the ’90s), and their backing of companies like Coinbase (who have announced the launch of “the first regulated bitcoin exchange based in the U.S.“) is part of a strategy to put in place the infrastructure and services necessary to support mass adoption.

Some believe that even if Bitcoin does not go mainstream, the Blockchain, secured by the Bitcoin mining network, will become the foundation for a multitude of applications and services like Blockstream, Counterparty, Factom, OneName and OpenBazaar. Overstock CEO Patrick Byrne has ambitions to build a distributed stock market on top of the Blockchain. This could result in a self-sustaining “cryptoconomy”, in which users buy bitcoins from miners, to spend on transaction fees (which go to the miners) required to write transactions to the Blockchain. The prospect of receiving those transaction fees would entice enough miners to maintain the security of the Blockchain. In other words, the intrinsic value of a bitcoin would be the ability to write to the Blockchain.

However, I think such a scenario, while possible, is unlikely. As I’ve said in the past, I doubt Bitcoin’s first-mover advantage will translate into long-term success. Webvan pioneered grocery delivery during the dot-com bubble but ultimately went bankrupt. Today, most supermarkets do deliveries, while companies like Ocado, Amazon and Instacart are resurrecting Webvan’s business model. I suspect that something similar will happen to Bitcoin and cryptocurrencies.

But it’s not happening just yet. Ripple, one of the early Bitcoin alternatives, suffered mixed fortunes in 2014. The circumstances surrounding the departure of co-founder Jed McCaleb (who had previously founded MtGox) to found Stellar, resulted in the resignation of Ripple Labs board member Jesse Powell, who highlighted the fact that Ripple’s founders hold significant amounts of the pre-mined currency. On the plus side, Ripple signed up three banks, including Fidor Bank in Germany and CBW in the US.

Other competing alternatives continue to emerge. Ethereum is intended to be a platform for smart contracts. MaidSafe is a platform for distributed storage, designed to support various applications. Storj is another distributed storage service that will compete with cloud storage services like Dropbox.

For me, the most important developments during 2014 were in the regulatory space. In the US, having warned Bitcoin exchange operators last year that they must comply with money-transmission laws, authorities began cracking down on “unlicensed money transmitters” (including BitInstant CEO Charlie Shrem and Robert “BTCKing” Faiella), as well as Bitcoin ponzi schemes and unregistered securities offerings.

In April, the IRS issued a notice indicating that virtual currencies are treated as property (as opposed to currency) for federal tax purposes and, hence, are subject to the rules pertaining to capital gains (and losses). This makes things rather complicated.

In June, New York’s Department of Financial Services (DFS) published a draft of its proposed “BitLicense” regime for regulating virtual currency companies, which attracted thousands of comments. A revised draft is expected imminently. Meanwhile, the Commodity Futures Trading Commission (CFTC) chairman declared that derivatives based on virtual currencies fall within the CFTC’s jurisdiction, and Circle (which launched its hosted Bitcoin wallet in September) was invited to join the Treasury Department’s Bank Secrecy Act Advisory Group.

On this side of the Pond, the UK’s tax authority issued guidance on the tax treatment of Bitcoin and other cryptocurrencies, and the financial regulator issued a Call for Information on Digital Currencies. Offshore, the Isle of Man government announced that it’s planning to create a regulatory regime that covers virtual currencies as part of a strategy to attract Bitcoin companies to the island.

Needless to say, the prospect of increased (or, rather, any) regulation of Bitcoin is not universally welcomed but it’s actually a critical step in laying the foundations for wider adoption of cryptocurrencies and related technologies. For example, there are doubts over Bitstamp’s solvency and security after it was hacked at the beginning of the year. If Bitcoin exchanges become regulated by something like the New York BitLicense (or, in Europe, in a manner similar to payments institutions, with appropriate measures for audit, security and segregation of client funds), it would go a long way to assuaging such concerns (not to mention make it easier for companies dealing in Bitcoin to get access to banking services).

In fact, I wouldn’t be surprised if 2015 is the year that being regulated becomes a competitive advantage for companies operating in the cryptocurrency space.

FIDOR Bank

Matthias Kröner from FIDOR Bank posted a response in the comments on What would a disruptive bank look like? which I thought deserved its own post.

Jack, it was absolutely thrilling to read your blog. Your blog and the – out of that – resulting discussion I really find unique. I am happy to participate in that particular discussion, because we build a real disruptive bank that corresponds with your criterias. The name of that Bank: FIDOR Bank.

How do I come to that bold opinion? Best proof would be to apply your criterias. So, lets see:

1. We are a real bank. We received banking license from the German banking regulators. That was in May 2009, so exactly in the eye of the crisis-storm and this as an entrepreneurial and independent team. No big banking group supporting (or blocking) us. We started business in Jan 2010 with a very rudimental offer.

2. From the start, our concept was designed exclusively for the digital market. By doing so, we focus on the main driver like Web 2.0, e-commerce, gamification and everything that comes around the mobile internet. We see absolutely no sense in a banking-branch, regardless of which bank. A branch is inferior to the Internet in all respects! For this I have also written a blog – but is currently available only in German. Sorry. Must translate that… Nevertheless, here is the link.

3. We have clearly opted for a banking license, because we had from the beginning on the opinion that one must have this license if you want to come to the core of a product and if you want to offer real innovation. The golden rule is simple: “Who wants to hijack a plane, should better sit in it.” (I am not saying, somebody should hijack a plane!!!! ;-))

4. If you hold no banking license, you only can focus on a (wonderful ) UX. That is it. Financial-Products and services are the ones which are made possible by the back-office bank and its core banking system. Not more.

5. We decided from the beginning to build our own middleware, because there was no suitable offer in the market. This is what we now call “Fidor operating system”. Out of that, Fidor TecS AG (a 100% subsidiary to the bank) as a company emerged. We see this fOS as the central tool to generate customer loyalty and stickyness. Our experience: If you work in the context of a concept that has the digital target customers (retail and SMEs) in its center and is not having its own technological expertise, you are lost.

6. Very Important: fOS is an “open” System. Via standard interfaces we integrate 3rd party offerings into our account. The result is as easy as compelling: A normal account has 3 functions: money in – money stays – money out. Fidor Smart Cash Account (as we call it) has already around 20 functions: In addition to the aforementioned , the customer may purchase foreign currencies and sell them and send them, also buy precious metals and sell and ship digitally, can order a mini credit via mobile app (we call it cash emergency) with an instant pay out even on a Sunday (our answer to wonga), can apply for an overdraft online and open it in seconds, can define saving certificates, may invest and participate in Crowd Finance as well as execute peer to peer lending , can use “social brokerage” offers, manage your card transactions in the same transactions-list like all your other transactions, and much much more. Not to forget, that we can integrate digital currencies into our account. Of course. That’s also the reason, why we are the only bank cooperating with two very active bitcoin exchanges. All that is creating a higher Customer engagement, a higher customer cross selling ratio and by that a higher customer life time value.

7. Yes, all that sounds like a complex account. But – in future – the customer can define his/her own account, like we do it today with our smart phone. That’s why we call it a Smart Cash Account. By defining your own complexity in that account, we integrate again the customer.

8. In addition, we operate a community, in which users can ask each other questions and give answers. Here you can rate products and consultants/advisors of all banks as well as you may wish to create products. Or you want to support other users by giving advice how to cut cost of living. Also you can compare your own financial profiles – of course anonymously. Naturally, we are active on all other social media channels and try to integrate the customer into the product also there. One example is our overdraft interest rate, that is driven by the numbers of Likes we have on Facebook. Easy rule: The more likes we receive, the lower the interest rate on the overdraft.

9. After establishing the first Fidor Hub in Germany, we now roll out internationally. We started in Germany, we now have a Russian franchise and we will come to market in the UK in the near future. 2015 it will go on like this, because Fidor has developed an international franchise concept.

10. In addition, one must see that we will connect these local franchise hubs in order to allow cost-effective real-time transactions between these local hubs then. Thats gonna be really cool and we will publish a press-release regarding a cooperation with a real disruptive partner in that segment in the near future.

And how do we manage all this? Well, we are currently a team of around 70 employees, unified by one mutual and super-important pre-condition: We have the right culture , the right spirit. Culture is therefore in a way more important than maybe the technology itself.

Did I forget something? Certainly …. yes. But, Jack, most important to me: you can tell Marc Andreesen and Chris Dixon that there is a really disruptive bank! That would be my only request… and wish ;-)) If I may be that open and frank.

Cheers

Matthias

Between FIDOR, the Open Bank Project and Avuba, it’s beginning to feel like the disruptive bank might come out of Germany, instead of the UK!

What would a disruptive bank look like?

A while back, I got into a to-and-fro on Twitter with Marc Andreessen and Chris Dixon about banking, which garnered a fair amount of interest and commentary1234, after Marc declared that he is “dying to fund a disruptive bank“.

So far, finance startups have shied away getting their own banking licence, opting to use an existing bank instead. Movenbank and BankSimple talked up their plans to shake up banking but, in the end, both dropped “bank” from their name and partnered with CBW Bank and Bancorp respectively (Simple was subsequently acquired by BBVA). In effect, they built a presentation layer on top of an existing bank. I don’t think that’s the path to the future of banking. Even if you ignore the downsides of building a business on someone else’s platform, I believe that you can’t be truly disruptive unless you build the full stack.

A bank can be broken down into two distinct businesses. The first is the infrastructure required to offer banking services: the banking licence or charter, branches and call centres (increasingly optional), IT systems, ATMs, AML and KYC procedures, connections to domestic inter-bank networks and SWIFT, the ability to issue credit and debit cards, etc. Some of these are revenue-generating (e.g. fees on SWIFT transfers, payment card interchange fees) but, traditionally, retail banks have offered “free” banking to attract customers so that the second business can offer them financial products like credit, overdrafts, loans, savings, investments, pensions, foreign exchange and insurance. This second business has attracted plenty of competition (including startups like Wonga, FundingCircle and TransferWise), but there appears to be little appetite for investing in the infrastructure required to become an actual bank.

The last company to do so in the UK was Metro Bank, which launched in 2010 (the first new high street bank to do so in 150 years) but has failed to make a make a significant impact on the incumbents’ market share (the top four UK banking groups have 70% of the market for personal current accounts5) and is yet to achieve profitability, having racked up over £150m in cumulative losses. With hindsight, part of the reason for Metro’s slow progress is the fact that, rather than trying to disrupt the market, it challenged the incumbents on their own turf by opening high street branches (26 so far, at a cost of over £2m each) and sought to compete on customer service (e.g. Sunday opening and welcoming customers’ pets into branches). Notably, it did not attempt to differentiate itself through technology, opting instead to outsource its IT to Swiss banking systems provider Temenos.

I believe that the technology platform can provide a strategic competitive advantage. As I’ve written before, the lack of competition in the UK market bred complacency and resulted in a failure to innovate and invest in technology (banks are notoriously reluctant to invest in something that doesn’t generate revenue unless it’s mandated by the regulators). As a result, the incumbents’ core banking systems are monolithic, clunky and ill-suited for supporting the kind of services that are made possible by modern consumer technology and connectivity.

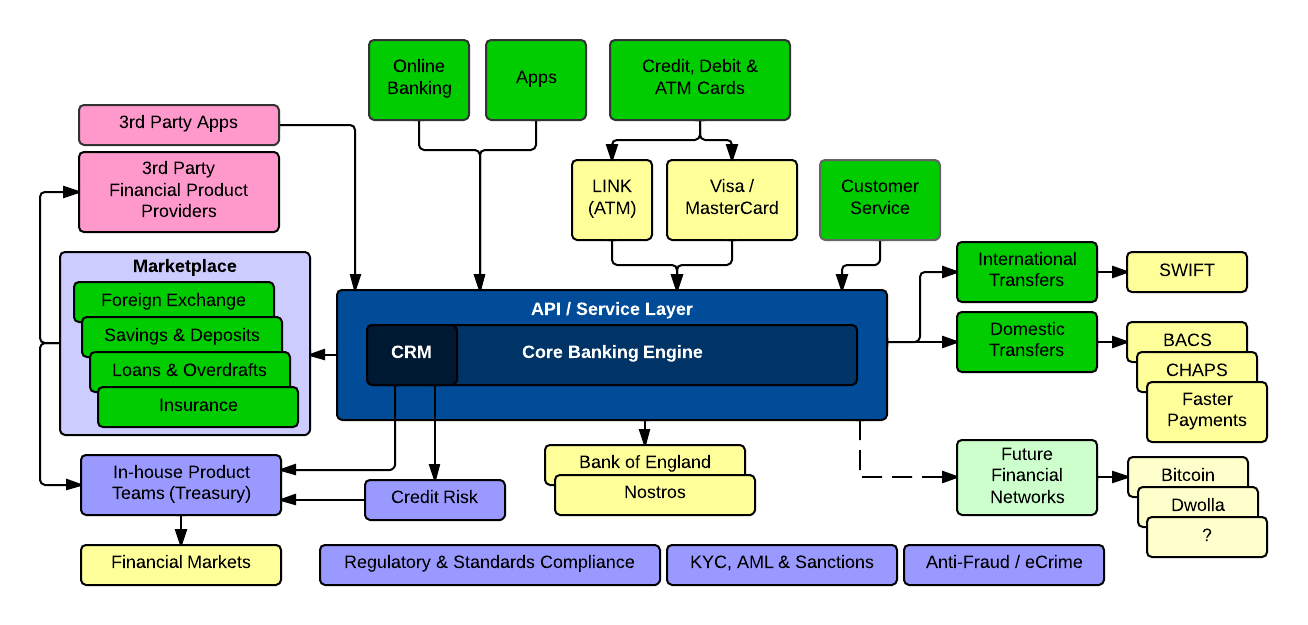

The ability to offer those kind of services would be a key differentiating factor but would require that the new bank build its own platform. I imagine it will look something like this:

A core banking engine, with integrated CRM functionality, wrapped in an API/service layer supporting online banking, and both in-house and 3rd party apps (e.g. personal finance managers, business accounting packages). Building a new engine from scratch, rather than using an off-the-shelf product, will allow the new bank to incorporate new features and functionality, like allowing customers to control which apps have access to their account (in a manner similar to the way Twitter lets you control which apps have access to your Twitter account) and set up IFTTT-style triggers. A modern platform will also make it easy to integrate with new financial networks.

Certain traditional banking services are prerequisites, such as payment cards, access to withdraw cash from ATMs and the ability to send and receive bank transfers both domestically and internationally. However, note the absence of any mention of branches, cheques or accepting cash deposits – all services that are expensive to provide and whose usage is declining precipitously.

Commoditised products like foreign exchange, credit and deposits are a competitive market and it’s easy for customers to access competitors’ product offerings, so it would make sense to create a marketplace where customers can get direct access to 3rd party products as well as those offered by the in-house Treasury product teams. In fact, providing a banking platform-as-a-service and white label services to other financial startups could generate significant revenues.

Efforts by UK regulators to foster competition in the banking market by encouraging more new entrants mean that now is probably the perfect time to launch a bank like this in the UK. In fact, last week brought the news that one of the co-founders of Metro Bank has teamed up with the former chief executive of First Direct (HSBC’s online and phone banking brand) to launch “the UK’s first truly digital bank“, although they appear to be following in Metro Bank’s footsteps by outsourcing the technology platform to Fiserv, a US financial technology provider.

The UK is arguably the best location for a disruptive bank to launch, with a financial technology talent pool that is probably the best in the world, and a sizeable addressable market that’s ripe for disruption. Once established in the UK market, a new bank will be well-positioned to take advantage of the single European market for financial services to expand throughout the EU and, with a tried and tested technology platform, it should be easy to attract the investment required to launch in the US.

The potential rewards are huge but so is the investment needed. Building a new technology platform and putting in place the support structures required is a major undertaking, not to mention the marketing spend that would be required to go mass market. VCs have become used to backing small teams of young technologists who build and launch a business over the course of a three month accelerator programme, or providing growth capital to companies that are scaling a proven business model. Whether they have the risk appetite for a disruptive bank remains to be seen.

- VCs Start Pining to Own a Bank at bankinnovation.net

- To disrupt banking, do you need to own the bank? at qz.com

- Financial interaction: the next generation by Roger Ehrenberg

- If you think ‘rip out and replace our systems’ is naive … think again at thefinanser.co.uk

- Calculated from the 75% quoted by the OFT in their January 2013 Review of the personal current account market less TSB’s 4.3% share after being spun out of Lloyds

Bitcoin Part 2 – The Legacy

“The test of a first-rate intelligence is the ability to hold two opposing ideas in mind at the same time and still retain the ability to function.” — F. Scott Fitgerald

I previously wrote about Bitcoin’s flaws. However, despite the fact that I doubt Bitcoin will succeed as a currency, I expect that it will leave a positive legacy. For all its flaws, Bitcoin has garnered far more usage and media attention than any previous cryptocurrency. That will have long-term ramifications, for a number of reasons.

Bitcoin Part 1 – The Flaws

When I return home from an overseas trip, I toss my left-over notes and coins into a drawer. Euros and US dollars obviously get used (as long as I remember to take them with me!) but the dirham, rubles, rupees, yuan, francs, and dollars from Hong Kong and New Zealand just sit there gathering dust – pieces of paper and metal that are effectively worthless here in London.

However, for all its faults, physical notes and coins remain the only way in which you can transfer currency in a decentralised fashion. Electronic money – the ones and zeroes in our bank accounts, the records of credit card transactions and inter-bank transfers – ultimately rely on central banks and mechanisms like CLS, which keep track of how much money each bank has.

Bitcoin is an effort to bring the advantages of physical currency – specifically the ability to transfer wealth with little-to-no cost and without needing to involve anyone else in the transaction – to the electronic medium.

(Many assume that Bitcoin transactions are anonymous. They’re not. All Bitcoin transactions are recorded publicly in the blockchain. At best, Bitcoin transactions are pseudonymous; at worst, network analysis – something that security and intelligence services are very good at – can provide major clues to participants’ identities.)

I first became aware of Bitcoin in 2010, when someone paid 10,000 bitcoins for a couple of pizzas. My instinctive gut reaction was that it was an interesting technology but, ultimately, would prove to be nothing more than a fad. Three years later, I have yet to be proven correct. Enough people have supported Bitcoin that an eco-system has built up around it. There are online exchanges where you can buy and sell bitcoins for dollars, euros or pounds; payment processors that allow merchants to accept bitcoins for goods or services; casinos where you can gamble your bitcoins; and online marketplaces where you can use bitcoins to buy drugs.